By Rachel Folder | Investment Analyst at NAOS Asset Management

It is our view that concentrated portfolios offer superior risk-adjusted returns over the long term. In this piece, we put forward the rationale for a concentrated portfolio and offer a discussion on some of the existing literature on the subject.

"A lot of great fortunes in the world have been made by owning a single wonderful business. If you understand the business, you don't need to own very many of them.” Warren Buffett

At the risk of oversimplifying, assume an investor has one really good idea, and implements it in two equally weighted portfolios – one portfolio holds 10 stocks and the other holds 100. If this good idea doubles in value, it will contribute 10% to the overall fund returns in the concentrated portfolio, but only 1% in the other. Of course, this is a very basic example, but it highlights the simple maths behind the idea that returns can be magnified through having more conviction in a few stocks, than less conviction in many.

Over the last 3 years to June 2018, 4 stocks in the ASX300 Industrials Index have been able to earn an annualised return of over 100%, and 15 stocks earned over 50% annualised return. Out of 219 stocks in this index that have been listed for 3 years, it shows how scarce really good ideas are. Our natural conclusion is that rather than investing in more stocks, what’s more important is choosing the right stocks.

Even if there were scores of great ideas available to investors, there are limits to how many an investor could implement well. Given the considerable amount of research and analysis involved in carefully selecting a good investment, one would expect the investor to spend a significant amount of time understanding the investment to have enough conviction.

If a fund manager holds a portfolio of many stocks, say for example 50, chances are the knowledge they possess about these stocks is lower than what a manager might know about their holdings if they held few, say 10 stocks. Focusing on a select number of investment ideas should allow a manager to capitalise on their knowledge advantage gained from following companies for longer, conducting more thorough research into the industry or competitors, and having a stronger relationship with a management team. Through this knowledge advantage investors ought to have a more thorough understanding of a company and use this to better identify mispricing opportunities in the market.

As custodians of others’ capital, we believe fund managers have a duty to not only grow this capital over the long term, but also to protect it. Holding concentrated positions can encourage a culture of risk management which focuses on downside protection. This can create greater motivation to avoid poor investments and deter managers from taking unnecessary risk that otherwise might be acceptable in a less concentrated portfolio. It may also steer the portfolio towards higher quality stocks.

There is no consensus in the investment community about what the optimal number of portfolio positions should be. However, the number of stocks you need to reap the benefits of diversification is probably less than you think. Benjamin Graham, the father of value investing, advocates for 10-30 positions. Seth Klarman, in Margin of Safety stipulated 10 to 15 different holdings provide sufficient diversification, Warren Buffet has suggested 5-10, while John Maynard Keynes has suggested 2 to 3.

A 2012 study by Alexeev and Tapon demonstrated that in the Australian market, a portfolio only required 14-30 stocks to reduce 90% of diversifiable risk as measured by standard deviation – supporting the argument that adequate diversification can still be achieved in a concentrated portfolio. While it is beneficial to reduce diversifiable risk (according to Modern Portfolio Theory, the market doesn’t compensate you for taking it) there is a turning point in practice where more positions may not necessarily mean greater returns.

Finally, and arguably the most important point for investors is how concentrated investing impacts performance. Funds investing in a higher number of stocks tend to have distributions of returns more closely centred around the market return when compared to more concentrated funds. In a 2016 publication, Concentrated Investing (Van Biema, Carlisle, Benello) the authors support this view through a study comparing return distributions from different sized portfolios, finding that the more concentrated the portfolio, the more chance of outperformance.

Specifically, a 10 stock portfolio had a chance of outperforming by 5% or more 2.6% of the time, compared to 0.1% of the time for a 25 stock portfolio and 0% of the time for a 30 stock portfolio. Of course, the corollary of this is that underperformance is also as likely; however, the analysis does demonstrate that the higher the number of positions, the more closely the fund returns match market returns, and to access returns that are different to the market, the portfolio has to be different or more concentrated versus the market.

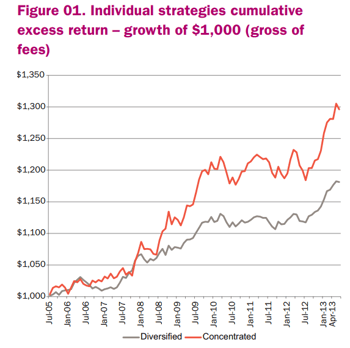

One simple analysis on the Australian market by Towers Watson found that concentrated managers outperformed diversified managers, in aggregate, over the period from 2005 to 2013.

One simple analysis on the Australian market by Towers Watson found that concentrated managers outperformed diversified managers, in aggregate, over the period from 2005 to 2013.

The evidence discussed here presents some persuasive arguments in favour of concentrated investing. But crucial in this is manager skill, and the ability for the manager to fight against common behavioural biases to take a sometimes unpopular view – and see it through to fruition. In our view, to balance risk and performance most favourably, the ideal number of quality companies in each portfolio would generally be between 0 and 30.

Read further insights by the NAOS team on The Importance of Corporate Culture Investing or Why Do Some Investors Underperform Their Fund Manager.

Important Information: This material has been prepared by NAOS Asset Management Limited (ABN 23 107 624 126, AFSL 273529 and is provided for general information purposes only and must not be construed as investment advice. It does not take into account the investment objectives, financial situation or needs of any particular investor. Before making an investment decision, investors should consider obtaining professional investment advice that is tailored to their specific circumstances.

Published: 8 August 2018

Join our investment community. Be the first to receive NAOS News, Insights and Invitations.