Robert Miller

The millions of people who tuned into the recent Berkshire Hathaway Annual General Meeting (AGM) were rewarded with an unexpected bit of news. When the question was asked whether the company would eventually become too complex to be managed by Warren Buffet, 90, and Charlie Munger, 97, Berkshire Hathaway Vice Chairman Charlie Munger made a comment that “Greg will keep the culture”. The question of who would take over after Buffett has been a source of speculation for over 15 years. Although Buffett gave no indication that he is planning to step down anytime soon, he has since confirmed that vice chairman Greg Abel will indeed succeed him as Berkshire Hathaway CEO when the time comes.

“The directors are in agreement that if something were to happen to me tonight, it would be Greg who’d take over tomorrow morning. We’ve always at Berkshire had basically a unanimous agreement as to who should take over the next day.” – Warren Buffett

Choosing a CEO is a high-stakes proposition, arguably the most important decision a Board of Directors can make. A CEO can have a significant impact on not only shareholders but also employees and their families, customers, suppliers and a wide array of other stakeholders. Flawed succession practices can lead to excessive turnover among senior executives and may ultimately lead to significant value destruction for companies (both qualitatively and quantitatively) and therefore investment portfolios.

Today, getting the CEO succession decision correct is potentially harder and more important than ever. Boards of directors, executive management teams, and CEOs face stricter regulatory requirements and higher customer/investor expectations, whether that be from an ESG perspective, a product/service perspective, or a financial perspective.

To successfully manage these challenges, it is imperative for a Board of directors to find a CEO with the most suitable qualities to tackle their company’s evolving strategic priorities.

In any given year, many Australian listed companies will undergo a change in CEO. This can be due to any number of reasons, which may include:

In the last 12 months, 35 companies in the ASX All Ordinaries appointed a new CEO (source: Factset). For these 35 companies, succession planning would likely have been a key priority of the Board’s agenda.

So, what are the secrets of hiring a great CEO? According to research produced by Australian specialist recruitment firm Robert Half, there are five key factors to consider when hiring:

While we can discuss each key area in length, the fifth factor being internal versus external is worth exploring in some detail.

“A company’s employees are its greatest asset.”

- Sir Richard Branson

Using the learnings from the Virgin Group founder, looking internally for succession is a logical activity.

There are a large number of benefits in appointing an internal CEO candidate, these can include:

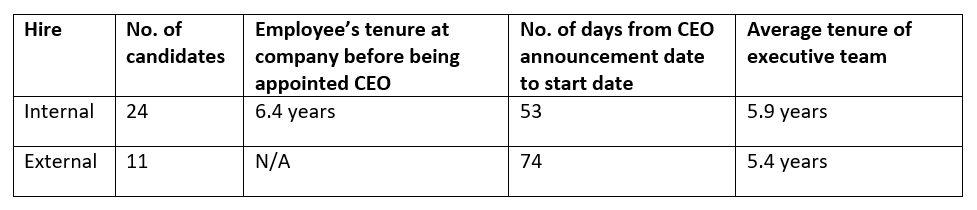

Of the 35 CEO appointments of ASX All Ordinaries companies over the past 12 months, the below table sets out some key statistics.

Regarding internally promoted CEOs, it is interesting to note the average tenure of the candidate prior to being announced as the new CEO was 6.4 years. Whilst the average tenure falls short of Greg Abel’s two decades with Berkshire Hathaway, it does support the Charlie Munger described the concept of being a proven performer.

Of the 24 internal appointments, the average number of days from announcing the new CEO to starting was 21 days shorter than an external person. This supports the abovementioned benefit that internally appointed CEOs are already across the ins and outs of the company and the transition period from outgoing to incoming CEO is likely to be a smoother process.

Finally, while it is difficult to assess a firm’s culture by looking at statistics, it is worth noting that across the firms that made an internal appointment, the average tenure of the executive team was 5.9 years. This was slightly higher when compared to companies that made an external appointment, being 5.4 years. A word of warning, there is potentially sample size bias given the 12-month timeframe.

Whilst an internally appointed candidate may have its benefits, on the other hand, it is potentially a disservice to shareholders and stakeholders if the Board simply have a narrow-minded approach and solely focus on an internal hire. Even though it might be difficult to ignore an internal candidate that might be a proven performer, hiring an external candidate can potentially fill some necessary gaps.

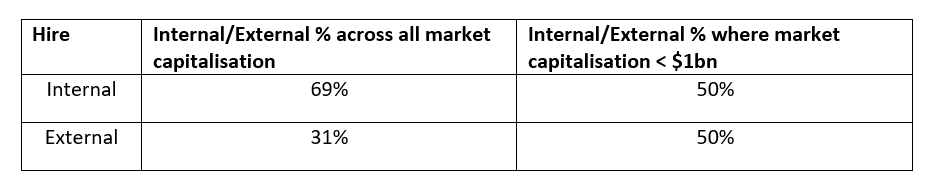

An external candidate can bring additional skills, processes, strategies and relationships that might not exist internally. This is sometimes common in smaller firms where the company might lack a deep talent pool. Across the sample size of the 35 companies, this was evident for firms that had a market capitalisation of less than $1 billion as per the below table.

For companies that are facing strong headwinds and need some drastic changes, an external appointment can be what is required, as they will likely bring a ‘fresh set of eyes’, may generally be more open-minded and may be less attached to the status quo of the current company strategy.

In other instances, an external candidate may exist who is of such a quality that they are going to be very desirable, regardless of the internal talent. For example, Richard Murray, who has been with the retailer JB Hi-Fi for 20 years, and CEO since 2014, was recently announced as the incoming CEO of Premier Investments. Murray is regarded as one of the best retailers in the market and has contributed to a total shareholder return (TSR) for JBH shareholders of ~24% p.a. since it listed in 2003, compared to the ASX All Ordinaries which delivered ~9% p.a. over the same period (source: Factset).

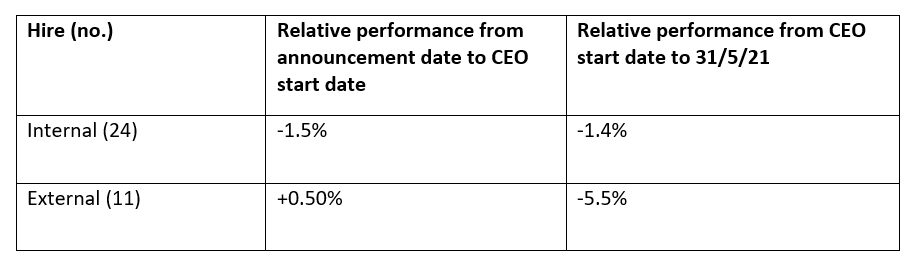

What has been somewhat surprising has been the market’s reaction to CEO changes. The below table summarises the performance from the ASX announcement date to the CEO start date, and performance from the incoming CEO’s start date to the end of May 2021.

In the short term, the market has clearly favoured external appointments. However, this has not been the case following the CEO starting, with the performance trend reversing and internal hires, although slightly underperforming the benchmark have outperformed their external counterparts.

Note – Benchmark used for relative performance is ASX All Ordinaries Index

At NAOS Asset Management, we invest in smaller companies and when analysing smaller companies, a CEO is likely to have an outsized level of influence over a company’s operations, culture, growth & strategic objectives. A critical part of our investment process is identifying the quality of a CEO. This is not a static process, rather a constant journey over the long term, which resets if/when a new CEO is appointed.

In our opinion, there is no right or wrong answer to whether a CEO should be internally or externally hired. What is important is that a Board of directors appoints the right candidate, for the right reasons, at the right time.

Livewire: Published 7 June 2021

Important Information: This material has been prepared by NAOS Asset Management Limited (ABN 23 107 624 126, AFSL 273529 and is provided for general information purposes only and must not be construed as investment advice. It does not take into account the investment objectives, financial situation or needs of any particular investor. Before making an investment decision, investors should consider obtaining professional investment advice that is tailored to their specific circumstances.

Join our investment community. Be the first to receive NAOS News, Insights and Invitations.