Regional NSW

At NAOS we include ‘hands on’ research as part of our investment process. Our job means we are fortunate enough to participate in site visits to various companies and stakeholders across a wide array of sectors and industries. From time to time, we will look to share a snapshot into some of the industry insights we learn from our travels on the road.

Regional NSW

A diversified construction, property and manufacturing business

Central West NSW

May 2022

Facts & Figures

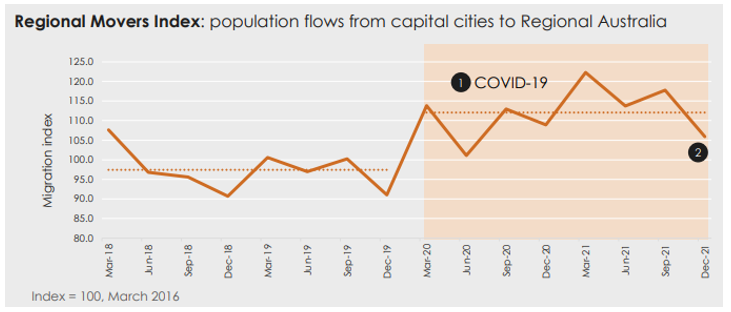

Covid-19 Impact

As governments locked down cities and CBDs, “tree changers” emerged and moved out of the big smoke and into regional and country towns as working from home took full effect. According to CBA Regional Index Movers, net migration to regional areas during 2020 and 2021 was more than double the level in the two years prior to Covid-19. Furthermore, during 2021, Sydney accounted for the largest net outflow compared to any other capital city and regional NSW saw its total share of inflows from capital cities increase to 50%, up from 36% in 2021.

Source – Regional Australia Institute

While the growth in regional NSW can’t be all prescribed to the above two factors, there are some interesting results from this strong net migration and a booming agricultural sector that are worth highlighting:

Source – Regional Australia Institute

Source – Regional Australia Institute

Infrastructure Projects

Since 2013, the Australian Government has invested in more than 750 major infrastructure projects and looking ahead, the Government has committed to investing more than $110bn over the next decade. Of these major projects, $87bn is taking place on the east coast of Australia over the next 5 years and $15bn will be spent in & around the Central West (within 1.5 hours of Dubbo). Whilst all these big numbers sound impressive, it’s worth diving into a few key projects to understand the scope and scale of these projects and the potential impacts they will have on the region.

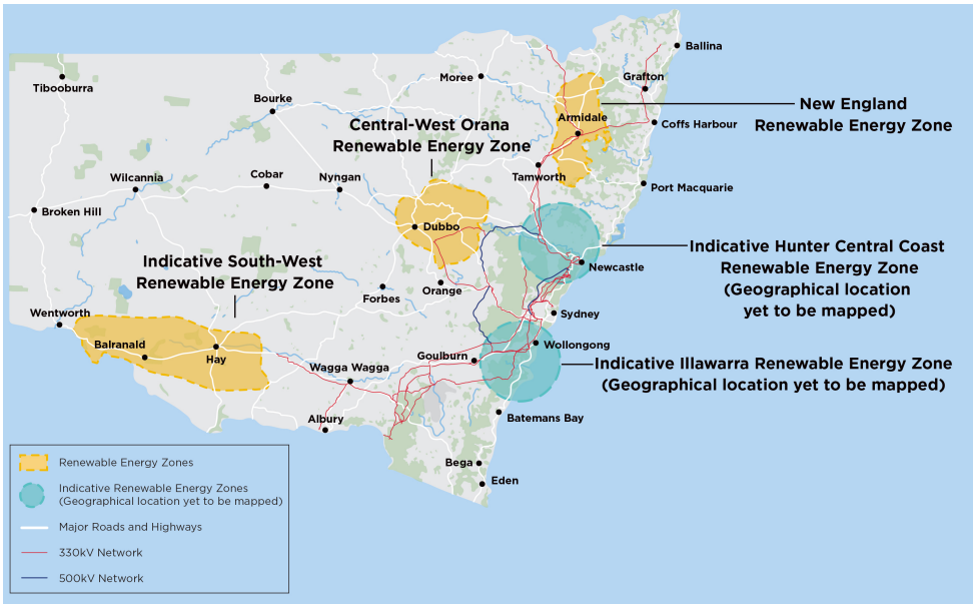

The NSW Government has embarked on a decisive plan to achieve its net zero carbon emissions by 2050 by creating five Renewable Energy Zones (REZ) across NSW. The objective is to help deliver affordable energy generation to replace the State’s existing power stations. The first pilot REZ will begin in Central-West Orana and will look to power 1.4m homes. Currently, the NSW Government has allocated $380m to the project. It is expected to create 3,900 jobs during the construction phase.

Despite the fact that Australia produced 20 million m3 of concrete and 5.6 million tonnes of crude steel in 2018, electrical generation and transmission only required one tenth of Australia’s steel consumption and nearly 1.3 million m3 of concrete, however this could significantly increase. One NSW case study found that the REZ programs could see steel volumes double and concrete consumption increase by 50% in the mid-2020s.

Source – EnergyCo NSW

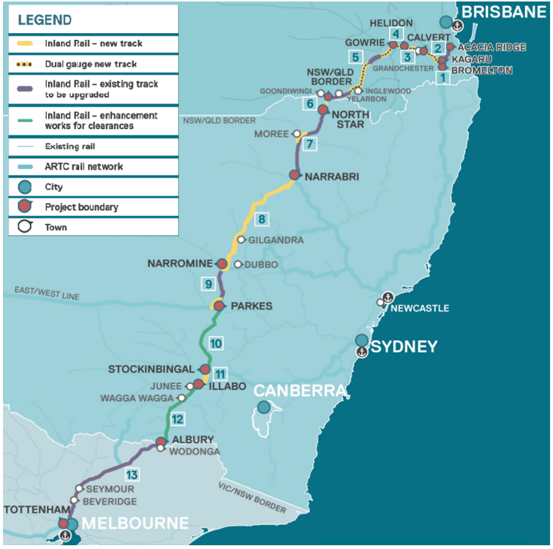

Inland Rail is a project spanning 1,700km of rail that will connect Melbourne to Brisbane. It will ensure the country keeps pace with increasing freight demand and provide support to businesses, farmers and producers and support a growing population. It’s a key initiative of the Australia Government’s $110bn infrastructure and roads upgrade program.

The project is made up of 13 individual projects across the three states with 1,100 kms of the existing network being upgraded or enhanced with the remaining 600 kms to be constructed. The project is estimated to cost $15bn.

Furthermore, it is estimated that the project will create ~20,000 direct and indirect jobs during construction. There is also the prospect of additional stages being added to the project in time (e.g. extending the rail up from Toowoomba to Gladstone).

Source – Inland Rail, ARTC

The NSW Government in conjunction with the Australian Government are investing close to $4.5bn (last estimate was updated in 2019) to upgrade the Great Western Highway between Lithgow and Katoomba.

The major road project will take approximately five years to complete, employing 3,900 workers during peak construction period. The upgrade, which is 34km, will complete the dual carriageway link across Blue Mountains.

While the final stage of the project is still in its infancy, NSW Government has just announced their preferred options for what will become the longest tunnel in Australia, taking commuters from Blackheath to Little Hartley. Early estimates are that the tunnel will save commuters 30 minutes off their travel time. Construction of the extension is expected to begin in 2023 and be operational by 2027/2028 lifting the total cost of the Greater Western Highway upgrade from $4.5bn to $8bn.

Office of Regional Economic Development (ORED)

Like a small country town that you didn’t knew existed but stumbled across on a road trip, we didn’t know that the NSW Government has an Office of Regional Economic Development (ORED). Established in April 2020, it is a fully dedicated regional investment promotion agency with the sole purpose of leading investment attraction, promotion, and strategy across regional NSW.

The sale of Snowy Hydro (by NSW and VIC to the Federal Government for $6bn) has created a once in a generation pool of capital which the ORED can deploy solely in the regions. The Snowy Hydro Legacy Fund of $4.2bn will sit alongside the Regional Growth Fund which had $2bn of capital as at April 2021, thus plenty of ‘fire power’ to drive growth. The focus of the ORED is on five key areas:

SAPs are regional locations identified to become thriving business hubs. In conjunction with external parties, the ORED will help plan, coordinate, invest and deliver key projects across these key SAP areas being Moree, Narrabri, Parkes, Snowy Mountains, Wagga Wagga and Williamtown. An extension of these SAP’s is to build Regional Job Precincts (RJPs) with four currently being investigated in Albury, Richmond Valley, South Jerrabomberra and Namoi.

Since the establishment of the ORED, it has facilitated capital investments of $561m and delivered job creation of close to 6000 FTEs. There is still a lot of ‘dry powder’ in the Regional Growth Fund and The Snowy Hydro Legacy Fund to be spent in the years ahead.

NAOS TAKEAWAYS:

As evidenced above, we are witnessing very strong interest in economies outside the major cities. Although it would be naïve to assume the “tree change” phenomena born out of COVID-19 continues indefinitely (given the trend’s short existence), it has certainly benefitted regional locations over the past couple of years.

On a much larger scale, the volume of infrastructure projects that will run for the next five to ten years is very substantial. These projects should attract not only workers but also businesses further into the regions. While interest rate increases might put a dampener on asset prices, the already low unemployment rates and extremely low rental vacancies should, in our view, create housing opportunities for many years to come.

All of the above factors will likely drive significant economic activity within regional NSW. How big that effect will be is yet to be determined.

APPENDIX:

5 Regional Economies

|

Economic Type |

Description |

Examples |

Population |

Employment |

|

Metro Satellite |

Relatively high-density communities on the outskirts of major centres of economic |

Gosford, Queanbeyan, Maitland, Kiama, Lithgow and Tweed Heads |

53% of regional NSW and has experienced above average population growth of 1.7% CAGR from 2011-2016 |

Gross value added of $105bn, with a growth rate of 2.1% annually from 2011-2016 Health and mining are key trade clusters, with 26,100 employees and 23,100 employees respectively |

|

Growth Centre |

Areas experiencing strong population growth and provide sophisticated health, education and cultural services to surrounding Inland areas. |

Bathurst, Orange, Tamworth, Dubbo, Lismore, Wagga Wagga and Coffs Harbour |

25.9% of NSW population reside in growth centres, and has seen population growth of 1% from 2006-2016 |

$44 billion in gross value added in 2016, driven by 1.3% from 2006-2016. Agribusiness is the largest trade cluster with 26,500 employees |

|

Coastal |

Supported by those aged 65 and over, coastal areas are more stable in terms of employment but are growing |

Clarence Valley, Far South Coast, Mid-Coast, Nambucca |

7.1% share of population, with less than 1% growth, mainly from those aged 65 and over |

Total gross value added in 2016 of $7.6bn, and annual growth of 1%. Key sectors include agriculture and health. Unemployment is generally higher than other regions. |

|

Inland |

Generally rural in nature and smaller but stable. |

Cowra, Western Murray, Mid-Lachlan, Murray, Northern New England High Country, Snowy Monaro, Snowy Valleys, South Western Slopes, Southern New England High Country, Upper North West, Western Riverina |

13.4% share of NSW population, with 0.3% growth from 2006-2016 |

Agriculture is the largest industry |

|

Remote |

Supported by agriculture and mining but is experiencing decline |

Castlereagh, Far West, Western Plains

|

1.5% of population but has been shrinking (-0.8%) |

Stable gross value added at $2.7bn driven mainly by agriculture |

Source – Regional NSW

Sources:

Regional NSW economies - https://www.nsw.gov.au/regional-nsw-today

Regional Aust Institute - https://www.regionalaustralia.org.au/Web/Media/Media-Releases/2022/Pandemic-Sees-Doubling-in-Net-Migration-From-Capital-Cities-to-Regional-Australia.aspx

Rental Vacancies – Central Tablelands - https://sqmresearch.com.au/graph_vacancy.php?sfx=®ion=nsw%3A%3ACentral+Tablelands&t=1

Regional Job vacancies – https://www.regionalaustralia.org.au/Web/Toolkits-Indexes/Regional-Jobs-Update/Updates/2022/Regional-Labour-Market-at-Full-Employment.aspx

https://labourmarketinsights.gov.au/regions/employment-regions-jobactive/?

EnergyCo - https://www.energyco.nsw.gov.au/renewable-energy-zones/renewable-energy-zone-locations

Inland rail - https://inlandrail.artc.com.au/what-is-inland-rail/

Centre of Population - https://population.gov.au

Office of Regional Economic Development - https://www.amgc.org.au/wp-content/uploads/2019/02/Murray-Wood-Office-of-Regional-Economic-Development-.pdf

Important Information: This material has been prepared by NAOS Asset Management Limited (ABN 23 107 624 126, AFSL 273529 and is provided for general information purposes only and must not be construed as investment advice. It does not take into account the investment objectives, financial situation or needs of any particular investor. Before making an investment decision, investors should consider obtaining professional investment advice that is tailored to their specific circumstances. This material may include data, research and other information from third party sources. NAOS makes no guarantee that such information is accurate, complete or timely and does not provide any warranties regarding results obtained from its use. Statements contained in this material that are not historical facts are based on current expectations, estimates, projections, opinions and beliefs of NAOS. Such statements involve known and unknown risks, uncertainties and other factors, and undue reliance should not be placed thereon.

Join our investment community. Be the first to receive NAOS News, Insights and Invitations.