The last twelve months can best be described as a game of two halves. The first half saw decent mid-single digit returns across equity markets, but the story dramatically changed in the second half as (amongst other things) investors came to terms with central banks quickly raising interest rates in an attempt to control inflation. But as investors close the books on what has been a difficult period for equity markets globally, attention now shifts to the upcoming reporting season.

|

|

S&P ASX Small Ordinaries |

S&P 500 |

S&P ASX 200 |

NASDAQ Composite |

|

FY22 |

-19.09% |

-11.09% |

-5.86% |

-23.52% |

|

1H FY22 |

6.10% |

11.09% |

4.51% |

8.06% |

|

2H FY22 |

-23.74% |

-20.47% |

-9.93% |

-30.07% |

Source - Factset

Given the financial year that it has been, we thought it would be worthwhile flagging a few key themes that NAOS Asset Management is keeping an eye on. It will look similar to last year’s (LINK), and while history doesn’t repeat but often rhymes, the next twelve months is shaping up to have a few surprises.

1: REALITY VERSUS EXPECTATIONS

While we have previously flagged that the two most common factors that determine market expectations leading into an earnings result are:

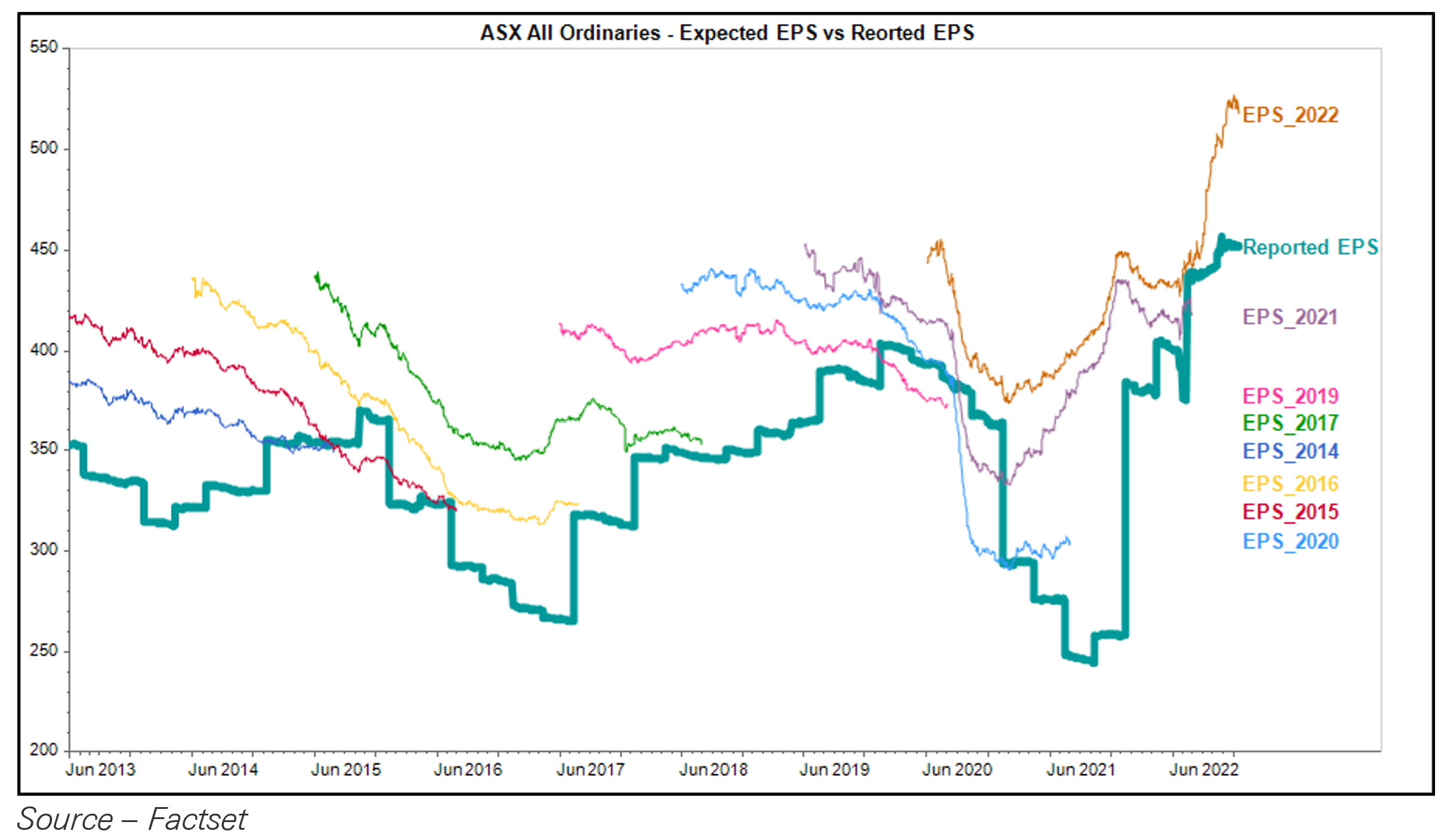

It is not uncommon for both of these numbers to differ, potentially significantly, from the actual result. The below chart outlines consensus EPS estimates per year (individual lines) and what was actually delivered (solid green line). As you can see, significant disparity exists in what was expected and what was delivered. The obvious trend here is that EPS estimates start high then slowly trend down as the year goes on. However, 2022 is clearly an exception.

In saying that, it’s worth noting domestic consumer confidence has been declining, similar to other OCED countries companies who benefited from a strong consumer balance sheet and sentiment might have some future headwinds. However, it’s worth remembering that the initial share price reaction on the day of an earnings announcement can be driven by a high level of emotion and not necessarily reflect the reality of the situation. We believe this can create opportunities for patient, long-term investors.

“Everyone has the brainpower to make money in stocks. Not everyone has the stomach.”

- Peter Lynch

Source – OECD, NAOS

2: CASH FLOW IS KING

In our view the best way to read a financial report is back-to-front – i.e. start with the cashflow statement and then work forwards towards the profit and loss statement.

Due to varying revenue recognition policies and accrual accounting, the profit and loss statement will not always give a true indication of what the cash earnings of the business have been during the period (e.g. capitalised product development spend). Free cash flow generation can provide a better understanding of this.

There is often a misconception that if profits are stronger then the company should be able to meet its financial obligations, however, it is not uncommon for a company to announce a positive profit figure, but the actual cash flow paints a very different picture.

3: RESULT QUALITY

At NAOS we like to focus on metrics associated with returns on capital and returns on equity. Whilst a static metric will give you a snapshot, often it won’t give you the full picture – trajectory is important. How does this year’s metrics compare to the last few years? Potentially of more importance is the trend of these return metrics and whether the company has options available to deploy excess capital at similar rates of return to how they have in the past.

A company with a relatively high but declining return metrics may be experiencing a decline in the quality of the business and its competitive positioning. Equally, increasing return metrics may highlight that the business fundamentals are improving. A business which is continually seeing increases to its overall quality of earnings can have significant compounding effects for shareholders over time.

Similarly, we like to see companies that are showing evidence of margin expansion. While this can be difficult in inflationary environments, quality companies that display pricing power should be able to pass on a portion, if not all of the higher input costs, either maintaining or expanding margins. At the same time, a company with a high level of fixed cost base, should see a higher portion of revenue drop through to profit which has the potential to see a re-rating due to multiple expansion. It is during reporting seasons where the team at NAOS search for these key attributes.

4: WHAT HAS PREVIOUSLY BEEN SAID?

If you really want to understand a company, we find a great way to do so is to read company announcements from at least the last few years.

It won’t take as long as you think, and it will give you a very good idea about what management’s strategy looks like and how they have executed upon it. This point particularly relates to capital allocation with an emphasis being placed on the last year or so. During this time, it’s likely that management’s view and actions have potentially changed and changed again given the level of uncertainty caused by COVID-19.

Thus, it’s important to understand and determine if a management team has been consistent on their strategy, as this will help to ascertain if you are buying a quality company that has resilience.

At NAOS we believe that the messaging provided to investors by management teams should be consistent regardless of the business cycle. If a business is performing consistently well or consistently poorly, the confidence gained by investors of a transparent management team who stick to their strategy is an extremely valuable commodity.

5: WHAT DOES THE FUTURE HOLDS?

Finally, the outlook commentary provides us with details of what to expect from the company going forward. It is quite customary for market participants to suffer from narrative bias, in which participants find meaning and patterns to explain the uncertainty and simplify the current situation.

We will often place a healthy level of scepticism on companies providing guidance for anything more than a 12-month period unless they have a highly predictable earnings stream. An overconfident management team that sets expectations too high will likely set themselves up for a poor period of share price performance if they do not deliver. We prefer a conservative management team who are aware that business conditions can change, and the business cycle changes with it.

WHAT WE ARE CURRENTLY LOOKING FOR

Every reporting season is different. So, while the above checklist provides a useful starting point, there are a few key themes that we will be looking for throughout the August 2022 reporting season.

1: CAPITAL MANAGEMENT

At NAOS we like to align ourselves with strong management teams that have displayed prudent capital management through various stages of the cycle. So, while there are increased levels of uncertainty due to rising interest rates, dampened consumer confidence and the ongoing impacts from COVID-19 including supply chain issues, the free-flowing stimulus tap that supported markets previously has been turned off. The decision on where and how to allocate capital potentially got a whole lot harder given the current environment.

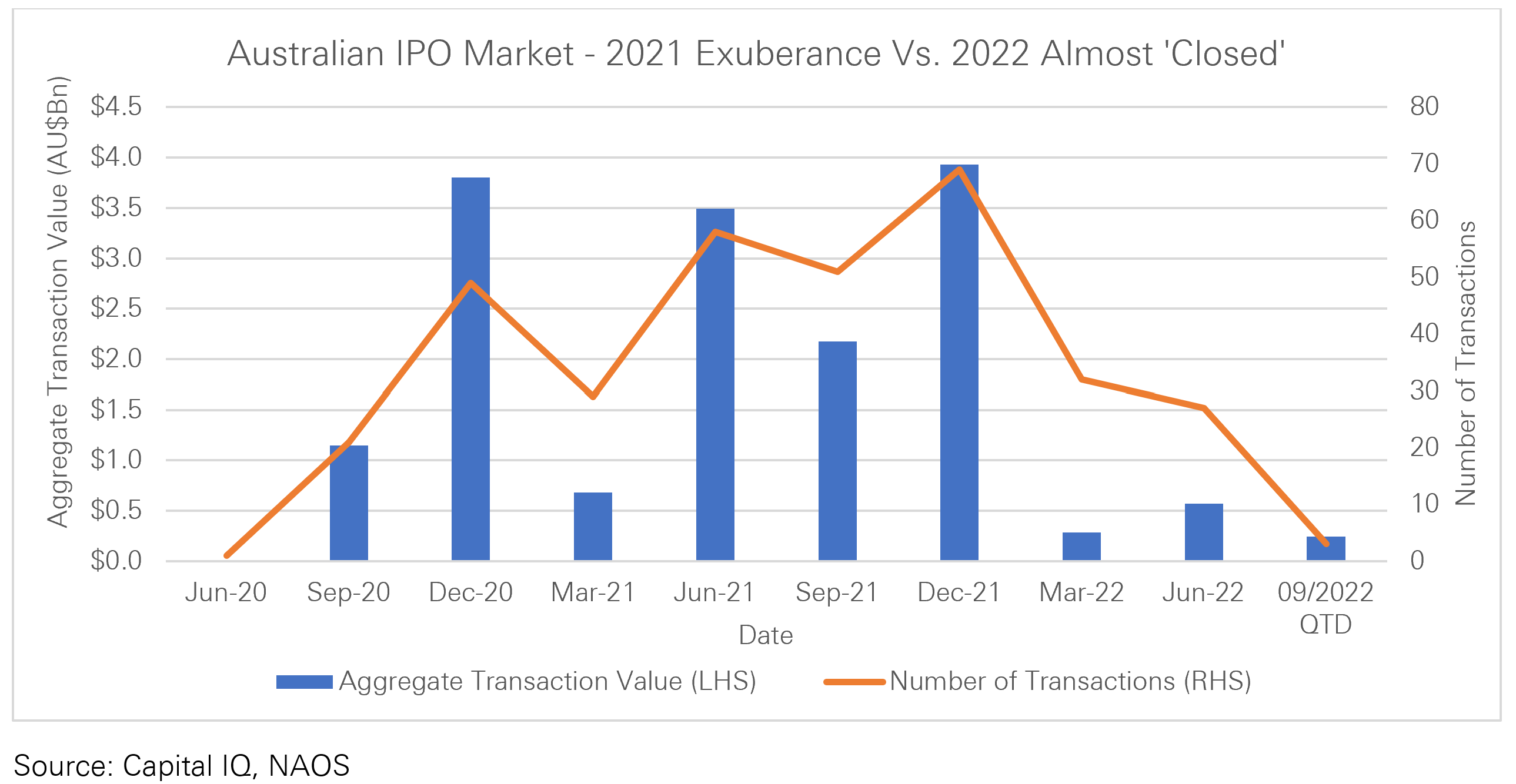

Very much a second half story is the decrease in IPOs (depicted in the below chart) and the compression in valuations. For management teams that might be looking to expand via acquisitions, the ability to raise capital at lofty valuations is very much a 2021 story, and accentuates the importance of a strong balance sheet with plenty of “dry powder”.

Another important part of the capital allocation equation is the topic of dividends. Something we are always mindful of is the relationship between a company’s earnings and their ability to pay dividends. We believe there is a risk, similar to what we saw at the start of COVID-19, of several companies either cutting or delaying dividends. Thus, we will be on the lookout for commentary around dividends, elevated or above average payout ratios, as well as commentary on growth and expansion initiatives.

2: COVID- 19 RELATED ISSUES

At the risk of sounding like a broken record given it’s almost two and a half years since COVID-19 first appeared in the headlines, the virus is still having an impact but it’s the second order effects that are worth keeping an eye on. A couple to mention:

(i) Inventory Levels

While the cost of shipping has fallen by ~40% from its peak in September 2021, its only down ~7% from the start of the 2022 financial year which is positive for heavy Amazon shoppers and companies that rely on importing or exporting either raw or finished goods. However, there is still a long way to go given the cost of shipping has increased 2.5x from July 2020.

A further reduction in shipping costs has the potential to provide tailwinds for margins however it’s the second order effect and the change in approach to inventory that is worth noting. “Just in time” has been replaced with “just in case” in which companies build sizeable inventory levels and attempt to anticipate demand levels.

Source – Freightos

However, given the cautious and increasingly pessimistic consumer, investors should be mindful of companies with large inventory balances.

(ii) Labour shortages

With borders closed, Australia’s unemployment rate has plummeted to 3.5%, the lowest it has been since August 1974, and it is estimated that there is currently one job vacancy for every unemployed person. While there are positives from a low unemployment rate, there are some consequences and impacts that investors should consider.

With a tight labour market, power now rests with the employee as employers struggle to not only recruit but retain staff. Companies are expected to increase wages at rates above CPI for key staff, but retention bonuses are being used to keep talent and, in some cases, sign-on bonuses are being used to entice new employees. This trend is taking place across skilled and unskilled workforces, with one interesting example outlined below, taken from Chatswood McDonalds.

Source – RBA & Australian Financial Review

Finally, given the shortage of both skilled and unskilled employees, there is a potential risk to some companies around their ability and capacity to complete work. It is hard to predict when the labour shortage pressures will be resolved but it is important to understand strategies that management teams are putting in place to address the issue and if there is any downside risk involved with the backlog of work some companies are facing.

3: BALANCE SHEET

At NAOS we have a preference for strong balance sheets with little to no debt as this provides a margin of safety and should allow a business to better navigate a crisis. While stimulus has been free flowing during the recent pandemic, interest rates are steadily increasing which will place pressure on companies and their balance sheets.

Investors should be mindful of a company’s ability to meet not only short-term but long-term liabilities, and emphasis should thus be placed on a company’s gearing metrics, overall debt levels and undrawn debt facilities.

“Cash combined with courage in a time of crisis is priceless”

- Warren Buffett

4: GUIDANCE

While guidance and company outlook statements are seen as important for forecasting future earnings, part of our investment process at NAOS is searching for companies that have an element of predictability in their earnings profile and can show resilience in all conditions. Although the risk of removal of future guidance has reduced, it’s important to understand the drivers of each company and key areas of risk.

The few examples that we have noted above, while might not be a comprehensive list are just a few things that we will be watching during the reporting season. Now every investor may have their own approach and areas of focus and while the challenging environment we all find ourselves in, this reporting season will no doubt present plenty of challenges but also plenty of opportunities. We at NAOS believe our long-term investment philosophy will allow us to take advantage of some of these opportunities.

Article Livewire: https://www.livewiremarkets.com/wires/the-results-checklist-and-what-will-be-catching-our-eye-this-reporting-season

Join our investment community. Be the first to receive NAOS News, Insights and Invitations.